Local content is often an emotive issue. It can get caught-up with ideas about identity and complicated by political positioning. The noise around local content can drown out any proper policy analysis.

This is why the Energy Chamber has placed a firm emphasis over the past few years on trying to put together an objective and transparent system to measure local content in Trinidad & Tobago.

As things stand today, upstream operator companies have an obligation to report to the Ministry of Energy on their local content policies and how they have performed. Unfortunately, these confidential reports to the Ministry of Energy are only ever reviewed internally and there is no system to aggregate and share the information submitted with wider industry stakeholders. The reports are not even reviewed by the Permanent Local Content Committee (PLCC) established under the 2004 Local Content and Local Participation Policy and Framework (which remains the guiding policy document for local content in Trinidad & Tobago).

As a long-standing member of the PLCC, I find this very frustrating. How can we guide local content policy if we do not have access to any data? However, instead of just complaining I have been trying to find an alternative way to address this problem.

The lack of a proper system to report and analyse local content was recognised by the Energy Chamber back in 2017, when we brought industry players together to sign a Charter committing to a series of actions on local content, including a system to ensure transparent measurement and standardised reporting of progress in respect of local content delivery. Coming out of this commitment the Energy Chamber has developed a Local Content Management System (LCMS), based on extensive consultation with both service companies, operators, and other industry stakeholders. My hope is that this system, now fully entrenched in the industry, can become the basic tool that is used to measure and monitor local content.

How does our LCMS work?

The heart of the LCMS is a detailed questionnaire filled out by companies who sell goods and services to the energy industry in Trinidad & Tobago. This questionnaire is designed to determine what percent of the spend by operators with these companies is retained in the local economy. The system is based around the “value retention” definition of local content that is included in the Trinidad & Tobago public procurement legislation, and which has also been adopted by the PLCC and the Energy Chamber through the Local Content Charter.

The “value retention” definition contrasts with the definition used by some other countries (for example Guyana) that places the emphasis solely on ownership and employment. With the mature energy service sector present in Trinidad & Tobago, the value retention approach, which concentrates how much of the spend of operators circulates in the local economy, was determined to be the more appropriate system by our stakeholder engagement process used to design the LCMS.

Over the past year we have gathered extensive data through the LCMS and we now have 482 companies who have submitted their questionnaires. The data coming out of the system is showing some really interesting patterns and highlights some of the important issues that we face in trying to maximise the retention of value in country,

As would be expected, there is a range in the local content scores obtained by service companies operating in Trinidad & Tobago. We have grouped the companies into tiers (1 through 4) and as Graph 1 shows there is a distribution among service companies reflecting different amounts of value retention.

Graph 1: LCMS distribution

Service companies and contractors who have managed to achieve the highest scores are those who are mainly providing services which do not require large investments in equipment and/or raw materials or consumables sourced outside of Trinidad & Tobago. The most commonly listed service in the tier 1 companies was civil engineering services

By contrast, the most common services listed by companies in tier 3 & 4 were services which rely upon expensive equipment, including the provision of equipment. As most of this equipment has to be imported, these companies have a lot of costs associated with providing this equipment. The table below shows the top five services or supplies listed by companies in each tier.

Table 1: Most popular services by tier

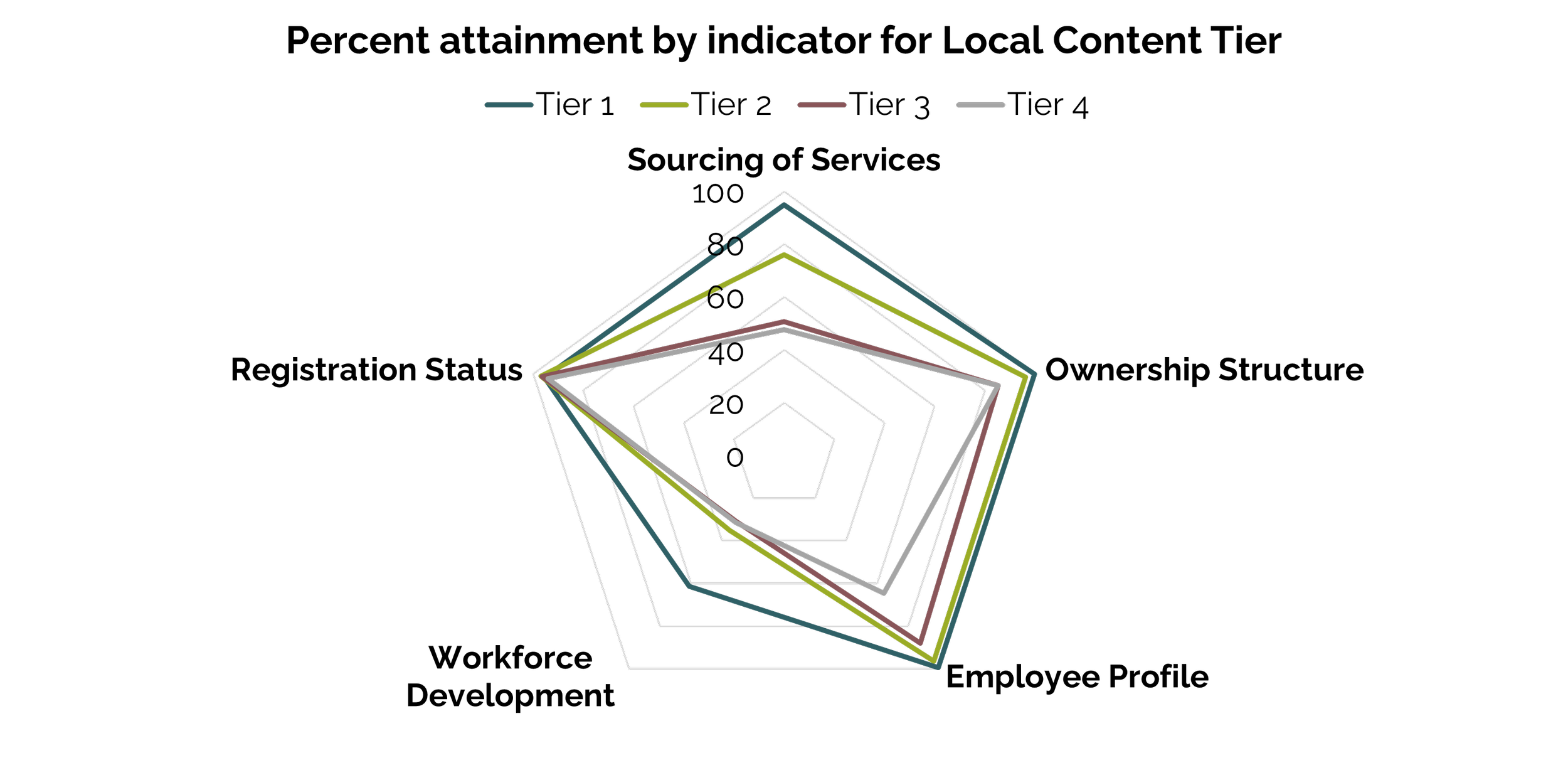

As Graph 2 shows, companies in tiers 1 – 3 have less variation on average in their scores for ownership and employment (and everybody does well in terms of company registration scores), and what sets them apart is the percent of their inputs that they have to source locally.

Graph 2: Percent attainment by indicator for Local Content Tier

Insights from the LCMS Data

It is clear from this perspective that restricting operators’ ability to procure goods and services to only locally owned companies will not have much of an impact on the value retained in the economy. The focus should instead be on making sure that there is a well-developed system of suppliers operating within the country and identifying goods and services that are currently imported that could instead be sourced locally. Some additional value can also be retained through prioritising local financing, which is one of the factors measured in the LCMS.

With the rapid growth of the energy sector in CARICOM there may also be significant opportunities to maximise the retention of value in the region if equipment could be more easily moved between the three main markets of Guyana, Trinidad & Tobago, and Suriname. I know it seems a bit counter-intuitive, but removing barriers to the free movement of equipment around CARICOM could actually help boost value retention in all economies of the region.

I hope that a more analytical, data-driven approach to local content can help develop the policies that are needed at the levels of specific companies, the overall industry, national governments and at a CARICOM level. The LCMS is a good place to start.