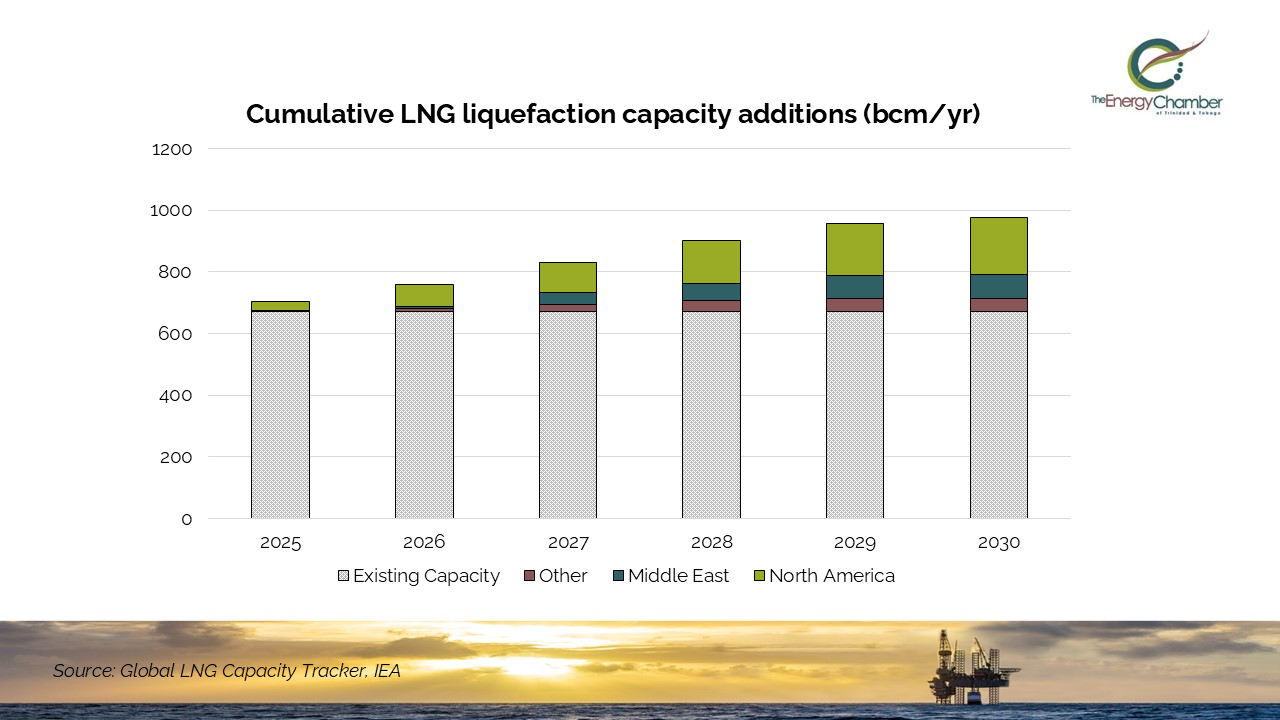

The International Energy Agency (IEA) has been tracking final investment decisions (FIDs) for new LNG export projects across the world and has published liquefaction capacity additions through 2030. At present, liquefaction capacity is approximately 670 bcm/y but between 2025 and 2030 it is expected that more than 300 bcm/yr of new LNG export capacity is expected to come online from projects that have already reached final investment decision (FID) or are under construction, marking the largest wave of capacity additions to date.

The largest set of additions comes from the North American region. It is anticipated that in 2030, 184 bcm/y will come from this market. Of this, 82% will come from the USA, while 14% will come from Canada and about 5% is projected to come from Mexico. The other major regional contributor to liquefaction capacities is the Middle East, which will account for almost 80 bcm/yr of new liquefaction capacity. The majority of this will come from Qatar (82%), the UAE (16%), and Oman (2%).

The global gas market is now on the verge of a new wave of LNG supply, driven by a surge in final investment decisions (FIDs) since 2019. The 96 bcm/yr of new liquefaction capacity sanctioned between January and October 2025 already represents the second-highest year for LNG FIDs on record.

The United States has been the dominant driver of LNG liquefaction project FIDs, accounting for more than half of the total since 2019. Qatar is a distant second with less than 20% of total FIDs, while the remaining 30% is distributed among roughly a dozen suppliers in the Middle East, Africa, North America, South America, Asia Pacific, and Russia.

According to the IEA, in recent years there was a significant reconfiguration of the geographic distribution of LNG FIDs. In 2022–2023, final investment decisions were dominated by North America, which accounted for three-quarters of sanctioned capacity. This was led by the US, which alone represented 70% of total FIDs, thanks to record-high prices and strong buyer interest in securing additional capacity from a flexible supplier. In 2024, by contrast, more than 70% of LNG FIDs came from the Middle East, while in the US there were no final investment decisions. This was due to a combination of cost inflation, concerns about medium-term market oversupply, and a temporary pause on LNG permit approvals. In 2025, new LNG FIDs began to return to the United States following the lifting of the permitting pause in January.

In Trinidad and Tobago, there were four LNG trains, but train 1 is currently being decommissioned due to gas supply constraints. The global increase in LNG demand highlights the continued potential for liquefaction and export of gas, once gas resources are available (either from domestic sources or pipelines imports from Venezuela or elsewhere). LNG remains a valuable commodity for which the government receives substantial revenue, and remains our major source of foreign exchange through exports.

While these trends point to an increased supply of LNG in the global market, many LNG and natural gas outlooks also project long-term growth in demand. ExxonMobil recently released its annual Energy Outlook 2025, which projects a significant increase in global demand for natural gas over the next quarter-century. According to the outlook, natural gas use is expected to rise more than 20% by 2050 compared to last year's levels. The LNG market is projected to double by 2050 as global gas demand grows.